Portugal Seeks Easing in Bailout Terms – WSJ.com.

The eurocrisis tends to divide into two camps. One side supports tax increases and budget cuts to close deficits, while the other is against this method. As one often finds during bilateral disagreements, both sides have merit in their arguments while a third choice outside the mainstream structure remains unexplored.

The only way to reduce a deficit is to eliminate the gap between revenue and expenditures; however, during an economic crisis government spending cuts leads to even greater decreases in GDP reducing revenue thus. This dynamic is known as the multiplier effect, which creates the pernicious debtor’s trap explained by Irving Fisher, “The more debtors pay, the more they owe.”

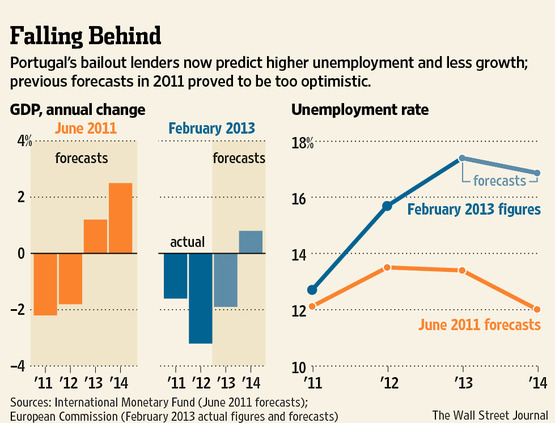

Economic forecasters from the IMF and Eurozone fail to take the extreme multiplier effect into account when making predictions. The attached graph show how badly they miss, and this is also the case in Spain and Greece. Note that the IMF has revised its forecasts for Portugal downward for 2013 and 2014, but if history is a guide they will miss again.

Austerity is not a way to help these countries but merely serves as political cover for their bailouts so as not to anger voters in Germany and the other creditor countries. While countries receive aid, they are punished for it. Portugal, Greece, Ireland and Spain, soon to be joined by Cyprus, are given just enough aid so that they do not default and exit the eurozone, while their economies continue to contract.

Just like Greece and Ireland, Portugal is requesting more time to pay its bailout loans pushing even more of today’s debts to future generations. The Germans will approve the request in order to maintain the eurozone for a little while longer ensuring Portugal remains in depression.

The Portuguese have only themselves to blame. By continuing to belong to the euro, they doom their country to years of economic stagnation.

You must be logged in to post a comment.