Disparity between the haves and have-nots in the Eurozone banking system.

Euro-Zone Bank-Rescue Deal Faces Hurdles – WSJ.com.

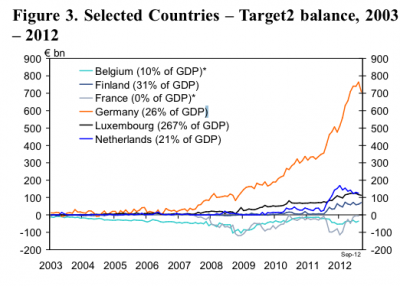

It was only two months ago that the mainstream media was proclaiming the start of the eurozone recovery with banking unions, green shoots and everything. Frequent readers of this site knew that the banking union was just hype, because the countries continued squabbling over the most important component of the banking union— the money.

A true banking union like that existing in the United States would assist in ending the the sovereign and financial sector link that has already bankrupted Ireland, Spain, Cyprus and Greece and threatens to take down other countries.

During the Great Depression, bank failures exacerbated the economic slowdown in the U.S. The regulatory model was failing, and a new framework was needed to break the link between failing banks and the poor economy, similar to the situation in Europe today.

Each state was responsible for regulating its own banks. Some states imposed strict capital requirements and sensible rules on their banking sectors, while others used a laissez faire approach. Officials soon realized that no matter how healthy their own banks were, failing banks in other states would drag down their institutions. The solution was centralized regulation with a depository insurance scheme and resolution authority paid for by all of the states through the federal government in the guise of the FDIC and the old FSLIC.

The Europeans cannot agree on a version of the FDIC, the indispensable piece of a banking union. Americans are one people, and states do not mind being joint and severally liable for each others debts through the federal government. Europeans do not share the same solidarity. While the debtor countries would love to have Germany and the northern tier on the hook for their banking systems and large government debt load, these countries are reluctant to share their surpluses.

During the June Euro Summit, the eurozone supposedly agreed to a banking union with joint and several liability among the countries. The plan was to allow the ESM to recapitalize failing banks directly so that the bailout money would not raise the debt to GDP ratios of the effected countries.

Three months later, the Bundesbank head, Jans Weidmann, began giving interviews stating that countries could borrow from the ESM for bank bailouts but would be liable for the costs. This was an important change of course, because it left the bank-sovereign link in place.

Germans believe that private investors should shoulder the losses for bank failures. Their concern is that removing the liability from countries for their bad banks creates the incentive for them to inflate credit bubbles, the moral hazard problem.

Eurozone officials have begun towing the German line:

Asking for direct recapitalization by the ESM would be regarded by the markets not as a sign of financial strength of a certain sovereign, but that the sovereign is signaling “I need some outside assistance.”

These reasons are merely pretexts for the creditor countries refusing to pay for the scheme. Currently, the ECB has LTRO and OMT programs in place, which are keeping ailing banks afloat. These programs both create moral hazard and have the potential to signal that the banks are weak, but none of the creditor countries object to these actions, because turning on the money machine appears to be free. Voters are not getting angry at ECB handouts, because they do not understand that they are on the hook for this money just as they are when their countries promise to contribute to the ESM, EFSF or some other euro-scheme.

Stark political calculus determines exactly what the creditor countries will continue to do. They will allow the ECB to use the printing press to maintain the current eurozone stability but will not overtly contribute additional sums. That is why you will never see a banking union or joint eurozone bonds.

As soon as monetary policy proves to be insufficient to maintain stability, the northern countries will have a choice to make. They will either have to assume the liability for trillions of dollars in debts from sovereigns and banks in the periphery or allow the eurozone to dissolve. While Super Mario has vowed to do “whatever it takes,” Merkel has yet to utter or back up a similar pledge.

Here are all of the links for prior banking union articles. They will quickly bring you up to speed with this part of the eurocrisis:

Germans Delay & Water Down Banking Union

European Banking Union Delayed and Unfunded

No Agreements on Euro Banking Union

Negotiations Ongoing on Euro Banking Union

Germans Will Not Pay for Banking Union

Cosmetic, Can-Kicking Banking Union Agreement in Play

Taxpayers to Pay Trillions for Banking Union

You cannot have a true banking union

without first establishing

a true tax union

and without first establishing

a true “enforcement mechanism” whether by arrest or confiscation or both.

While you may give money,

we all know it is very likely it will not be paid back unless payment is forced.

And you cannot force, where “bribery” or “political favor” in one

Country, means citizens can never be arrested and/or property confiscated for payment.

In a rush to euro the money, they never (tried as they did) came to agreement

on tax or enforcement.

They knew these were required; but they could not get agreement.

Instead they wrote, in effect,

if someone breaks the rules we will write new rules later.

It was destined for failure from the start.

It is rather funny because I can imagine the conversations being held right now:

EU we loaned you money we would like it back

GK ah, we spent it and we have no money

EU oh, hmmmm.

GK can you loan us some more money

if you do we might be able to pay you back in a few years.

EU where did the money we gave you go

GK oh we gave it to some banks

the bank leadership took millions in salary and bonus

the banks invested with several crooks that stole hundreds of millions

one of the bank representatives and family embezzed millions

it is all gone

EU well can we tax the salary and bonus

GK oh Im sorry, we have a hard time collecting taxes, try as we may

EU well can we arrest the embezzler and the crooks

GK oh, Im sorry they are very respected citizens

EU oh, hmmmm.